Key Takeaways

- MFN pricing is accelerating U.S. drug price compression earlier in the lifecycle.

Through Medicare GLOBE and GUARD, pricing pressure may emerge in the first 1–2 years post-approval, far earlier than IRA negotiation timelines, linking U.S. net prices more directly to lower OECD reference markets. - Global launch, valuation, and evidence strategies must now be designed around pricing risk, not added later.

Executives must integrate pricing governance, clinical evidence planning, and reimbursement positioning from Phase 2 onward to protect long-term value across U.S. and ex-U.S. markets. - Passive or defensive responses are unsustainable, proactive governance and policy engagement are required.

Biopharma leaders must actively monitor policy evolution, shape regulatory dialogue, and implement structured price governance frameworks to retain strategic control in an MFN-driven market.

Target Audiences

Innovative Biopharma Executives (US)

Executives with assets in early stages of development or nearing US FDA approval, as well as those seeking ex-US launch partners.

Big Pharma Executives in ex-US Affiliates

Executives who are part of the OECD19 and simply trying to understand the pressures being faced by their global and US colleagues, and anticipate global launch governance pressures from the center.

Call to Action

Discover the strategies helping pharma and biotech leaders respond to MFN-driven pricing pressure with clarity and control.

Overview of the US MFN Situation

In May of 2025, the Trump Administration issued an Executive Order aimed at ‘Delivering Most-Favored-Nation Prescription Drug Pricing to American Patients.’

The order states the “Administration will take immediate steps to end global freeloading and, should drug manufacturers fail to offer American consumers the most-favored-nation lowest price, my Administration will take additional aggressive action.”

The order promised within 30 days to “communicate most-favored-nation price targets to pharmaceutical manufacturers to bring prices for American patients in line with comparably developed nations”

MFN has been a clear policy ambition of Trump administration since his first term. The belief that other wealthy markets are “free riding” off US prescription drug prices was hotly debated and early pilots stalled. But in under a year we have transitioned from the issuance of the MFN Executive Order to confronting four key initiatives that are likely to disrupt US and global drug pricing forever:

Federal Government Deal-making: The executive order came with a requirement for top tier big pharma companies to meet with the federal government and discuss deals to align key parts of their drug portfolio prices with ex-US wealthier market prices. Most dramatic among these meetings were the deals made with Lilly and Novo Nordisk on their GLP1 diabetes and obesity assets. In some cases, newly approved innovative assets as part of the new CNPV are having negotiations with MFN even before formal FDA approval. See our recent MOMENTUS Perspective articles on these topics.

GENEROUS – Medicaid. Voluntary MFN-based program to enhance Supplemental Rebates per MFN price comparisons and enable broader, nationwide Medicaid access.

GLOBE – Medicare. Mandatory MFN Pilot for Medicare Part B patients and drugs.

GUARD – Medicare. Mandatory MFN Pilot for Medicare Part D drugs (includes beneficiaries in standard Part D Plans and Medicare Advantage).

In this piece we focus on the two new Medicare MFN pilots as they stand to be the most disruptive to drug pricing in the US and global markets. The GENEROUS program is voluntary and is estimated to offer minimal additional price reductions given that Medicaid net prices for the most part are already close to European levels.

GLOBE & GUARD

Both apply to US beneficiaries in Medicare, the program primarily for people over the age of 65 years. Biopharmaceutical companies developing therapies targeting older patients (eg, oncology, Alzheimer’s disease) will be most at risk.

GLOBE applies to Medicare Part B, for medicines administered in the presence of a healthcare professional, for example, infused cancer drugs.

GUARD applies to Medicare Part D, for at-home, self-administered drugs like oral solids (tablets, capsules, oral solutions) and subcutaneous self-injections.

These programs are distinct from the recent IRA Medicare Negotiation rule in that the pricing actions will apply once a product reaches an annual sales threshold of $69-100 million annually. This can occur as early as year 1 or 2 post FDA approval for select novel medicines. If more mature products have already been through the IRA Negotiation, GLOBE and GUARD do not apply.

See more details below.

Pricing Rules That Apply to Both Medicare MFN Pilots

- Mandatory, once surpassing annual Spending Threshold

- Testing in select Geographies of US (~25% of beneficiaries)

- Reduces price down to lowest price in basket of 19 OECD countries, adjusted for GDP per capita of US relative to lowest country referenced

- Drugs exempt if having already set an IRA Negotiation price (MFP)

- Single source brands with remaining exclusivity (not generics or biosimilars)

Comparison of Pricing Regulations in Medicare GLOBE and GUARD

| Category | GLOBE | GUARD |

|---|---|---|

| Medicare Segment | Medicare Part B (for physician/nurse administered drugs like intravenous (IV) infusions) | Medicare Part D (self administered / at home drugs like pills, subcutaneous self injections) |

| Start Date / Test Period | Starts Oct 1, 2026 and runs until Sep 30, 2031 (5 years) | Starts Jan 1, 2027 and runs until Dec 31, 2031 (5 years) |

| Spending Threshold | $100 million annual sales | $69 million annual sales |

| Drug Categories Subject to MFN Price Adjustment | Antigout, antineoplastics (cancer), blood products and modifiers, central nervous system, immunologicals, metabolic bone disease, and ophthalmics. Example (not subject to IRA negotiation to date): Keytruda, IV infusion for multiple types of cancers; ~$18 billion US sales in 2024. | Analgesics, anticonvulsants, antidepressants, antimigraine, antineoplastics (cancer), antipsychotics, antivirals, bipolar, blood glucose regulators, cardiovascular, central nervous system, gastrointestinal, genetic/enzyme/protein disorders, immunologicals, metabolic bone disease, ophthalmics, respiratory/pulmonary. Examples (not subject to IRA negotiations to date): Mounjaro, self injection for type 2 diabetes; ~$7+ billion US sales in 2024. Dupixent, self injection for immunologic/respiratory/COPD; ~$14 billion US sales in 2024. |

19 OECD Countries – Australia, Austria, Belgium, Canada, Czech Republic, Denmark, France, Germany, Ireland, Israel, Italy, Japan, Netherlands, Norway, South Korea, Spain, Sweden, Switzerland, United Kingdom.

GUARD: Guarding U.S. Medicare Against Rising Drug Costs

GLOBE: Global Benchmark for Efficient Drug Pricing

Why is Recent MFN Regulation So Disruptive?

- MFN Impacts innovative brands early in their lifecycle, possibly in the first 2 years, whereas IRA Negotiation does not take place for 9-13 years after the first indication FDA approval.

- OECD19 visible reimbursement prices are often significantly lower than US (see our past MOMENTUS Perspective blogs explaining why prices differ globally; reimbursement price can be up to 80% below US List) and will push US net price pressures well beyond those seen in the current system. Raising prices in Europe and other OECD19 countries is legally challenging and unlikely to occur without removal of reimbursement – leaving market withdrawal or cancellation of launch a serious consideration.

- Medicare Part B drug prices may take a big hit: This government segment has largely avoided price-access pressures until now. Medicare, by law in Part B, does not manage net price, formularies, or utilization controls like prior authorizations and step protocols. Unless there is a rare decision by Medicare not to cover an HCP administered therapy for lack of evidence (eg, aducanumab for Alzheimer’s disease in 2021). Medicare Part B typically covers HCP-administered drugs fully, according to label, upon FDA approval. Net price therefore is only reduced due to channel and reimbursement dynamics (340b, GPOs, etc). Thus, Part B drugs may have a long way to fall, and it is expected MFN,and IRA for that matter, will have their most dramatic cost containment impacts in Part B with big selling brands like KEYTRUDA.

- Newly negotiated US government prices emerging from the past year of MFN and IRA are breaking through traditional floors, and then made public which will inevitably provide new price floors for Private US Payers to reference. The entire US market may migrate to a new price floor possibly not far from current European levels unless global launch policy and strategy change.

- Big Pharma bellwether firms over the past year have demonstrated willingness to go to the Government Negotiation table, even for newly launching brands. Many have negotiated launch deals with the Trump Administration, often in conjunction with the new CNPV program from the FDA. Lilly recently agreed to a rock bottom price for its yet to be approved oral GLP1 as part of their MFN negotiation. This is opening a new door, sliding the US a bit further down the slope toward endorsing US government controlled launch pricing. Cabinet members in the Administration have been quoted as saying MFN policies will start with government sectors, but intend to move to commercial and private payers as well.

- Immediate, knee-jerk reactions by Innovative Biopharma Execs have included cancelling the launch of new brands in the OECD markets. This can be highly disruptive to the operations and profitability for European and other ex-US Affiliates. This also limits the global valuation opportunity for investors as they must recalibrate their models, possibly reducing downside scenarios to a US market launch only.

- Biotech Investors are conservatively weighing these complex new pricing regulations, and heavily altering their valuation and forecast models, perpetuating a stagnant biotech funding environment, and widening the door for China biotech global dominance in coming years

Concerned Biopharma CEOs, Boards and Investors find the safest path for now is to focus on commercializing in the US only, removing ex-US price referencing risk until the dust settles.

In our view, this is not sustainable. It likely does not make sense for many assets in the mid term horizon, and certainly is not a long-term global development and commercial strategy for a biopharma industry hoping to stay competitive in the future.

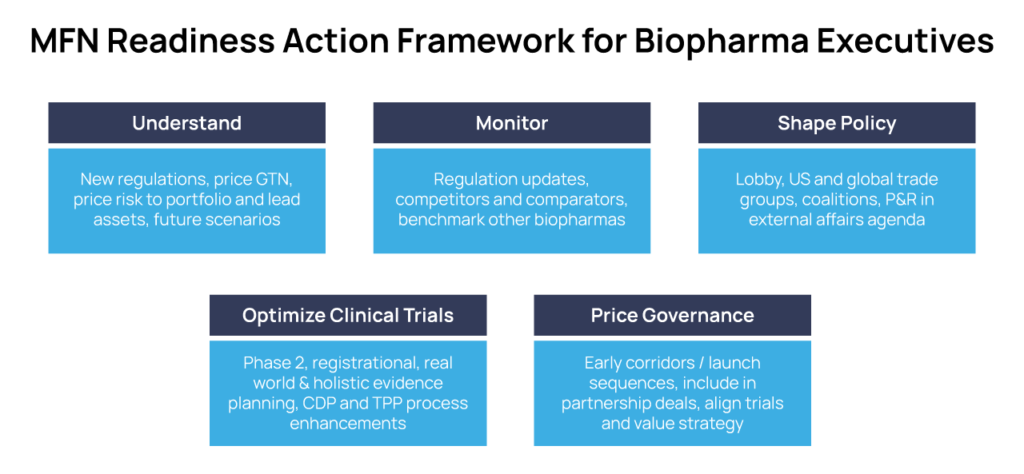

What is a Biopharma Executive to Do?

Policy advisors and law firms have boiled hundreds of pages of Regulations into simple, easy to understand breakdowns of each MFN pilot program (see example in Sources below). We do not regurgitate detail here, but rather aim to give practical guidance to executives regarding what you can do next, taking meaningful actions on your policy downloads.

We want to help you devise strategies now, even if your novel assets are 3-5 years from US FDA approval. This should enable Biopharma Leadership Teams to regain a sense of control, and begin to deal with MFN pricing uncertainty in a pragmatic way – moving beyond knee-jerk defensive actions, and developing a roadmap of initiatives to ensure price optimization in US and key ex-US markets.

KEY ACTIVITIES FOR COMMERCIAL DEVELOPMENT AND R&D READINESS

Understand

Immerse in, socialize, and align across your Leadership Teams the many detailed Legal &Policy overviews from your US and European Government Affairs and Market Access experts. Elevate this issue via your Chief Commercial/Business Officer, and discuss and align this threat at the highest levels of corporate governance.

Go deep. Understand price differentials in OECD19 and US for your asset’s analogues, competitors, and comparators.

Perform Gap Analyses and develop Risk Scenarios customized to your portfolio and lead assets – eg, are you in Rare Disease for pediatrics in Medicaid, or are you in Oncology with a large mix of patients over 65 years old? Are the comparator prices in your category at risk of large price adjustments, or is the corridor relatively tight?

Understand what drives Gross to Net (GTN) pricing waterfalls in US and OECD markets – public, list/ex-factory, reimbursement, rebates and discounts, off invoice discounts like 340b, etc.

Predict how recent PBM reforms and government regulations (Feb 2026) will change List >N pricing in the US going forward.

Model strategic scenarios – how will prices evolve before your approvals? how could the various MFN Pilots evolve into Law? How will ad hoc MFN deals relate to GLOBE, GUARD, GENEROUS and IRA Negotiation?

Monitor

Consistently generate intelligence on policy changes, price actions, and negotiations of competitors, comparators and analogues that will impact your entry strategy.

Benchmark MFN readiness actions of Big Pharmas and other biotechs – learn by example.

Shape Policy and Your Future

Be part of the lobby and trade groups in US and Europe; even with low budgets you can be part of BIO coalitions and have a voice.

Lobby in US for fair, transparent negotiation approaches [not back room deals] in any of the new programs and processes -ad hoc, IRA evolution, and CNPV.

Lobby European and OECD19 markets to allow Confidential reimbursement pricing arrangements; enabling a List/Visible price framework that minimizes US MFN actions

Shape the evolution of IRA and MFN regulations in ways that support US innovative biopharma investment and stay competitive with China’s surging biotech industry.

Predict your Asset Price & Reimbursement attainability in US and key OECD19 markets (eg, Germany, France, UK) early in development (Ph2 design in some cases). Conduct primary research with payers on your key Asset evidence, value and reimbursement potential scenarios, align across Clinical Development and Regulatory via real-time TPPs and CDPs.

Optimize Evidence: Guarantee Your Asset’s Value Differentiation with All Stakeholders

Interrogate your Asset’s CDP and TPPs. Ensure Ph2 and registrational trial evidence are ready for this new world of regulations and pricing & reimbursement negotiations. Re-define the optimal populations, comparators and endpoints for all key trials.

Update R&D and Clinical Development processes. Compel your Regulatory and Clinical Development heads and the ‘Program Team’ to infuse global price and reimbursement ‘readiness’ into their development strategies and plans.

Engage early in Real World Evidence planning and generation – before filing with FDA.

Define the key value drivers for you key Assets early in development, not at FDA approval

Prepare early to Negotiate value and price at Launch with the new US pricing bodies and procedures. US launch access hurdles now include: Medicaid (state by state, managed Medicaid, GENEROUS), Medicare (GLOBE, GUARD, Part D Health Plans), Commercial (PBM, Health Plans). With recent PBM reforms and regulations, we may soon add large Employers to this list.

Develop a Price Governance Framework for Your Assets

Price Governance Policies are not just for Big Pharmas with large portfolios, global staff and Affiliates all across the world.

Innovative biotechs/pharmas should have an Asset Price policy and plan, whether going it alone worldwide, or seeking ex-US licensing partners. It is important that licensing deals align with your price and value capture expectations worldwide.

Governance Frameworks should include — planning attainable list and net prices in US and Key global markets; setting guardrails (corridors, floors) that factor the new MFN and US P&R environment ; planning country Launch Sequences to optimize price in a new world of International Reference Pricing (IRP) across all key markets.

Sources:

MFN Executive Order, May 2025

Legal White Paper – Goodwin Law – GENEROUS, GLOBE, GUARD

CMS Most Favored Nation Part B Drug Pricing Model

Trump Blueprint to Lower Drug Prices

IRA Medicare Drug Direct Price Negotiation Provision – CMS Fact Sheet

Leave a Reply